In some places, housing cost often slip ten-20% because the home loan cost rise to cuatro%: BMO

Much of the main focus for the rising borrowing from the bank pricing has been on the way the extra financial weight tend to apply to normal mortgage payments having Canadian residents.

Much less attract might have been to the greater effect out-of high rates of interest having Canadians exactly who acquire about security inside their property courtesy contrary mortgage loans and you can house collateral contours out of loans (HELOCs).

New posted four-year repaired opposite financial price at home Collateral Lender, the key vendor of contrary mortgage loans for the Canada, have hit a close look-swallowing eight.35 per cent.

Opposite mortgage costs are normally higher than antique mortgage pricing; however, due to the character of reverse mortgages, high cost tend to eat out in the guarantee in the home and you may material overall desire payments over time. Having said that, old-fashioned home loan repayments reduce steadily the dominating and complete attention costs more than big date.

Opposite mortgage loans succeed home owners old 55 and old to use tax-totally free money against to 55 percent of one’s appraised value of their houses. Courtroom control stays to your resident nevertheless the loan amount and you will obtained focus need to be paid if the property is marketed otherwise moved, or in the event the homeowner passes away.

Once the term means, opposite mortgage loans act like old-fashioned mortgages – but instead of costs moving on the domestic, they disperse out. That implies rather than the prominent (amount owing) falling throughout the years, the principal rises over time.

Property security line of credit lets homeowners so you can borrow secured on the fresh new guarantee within property at often by just going dollars after they want to buy.

Borrowing from the bank limits should be to 80 per cent of your own home’s appraised worthy of, without one a good obligations to the first mortgage.

The speed toward HELOCs is frequently tied to the top lending speed at most banking companies plus the distinction can be negotiated. Should your rate are adjustable, not, the main could be more-sensitive to interest rate develops. Occasionally, https://cashadvanceamerica.net/loans/variable-rate-loans/ a loan provider will give repaired-title house equity money more certain time period including good conventional financial, but HELOC cost will always be susceptible to rising interest rates if the dominating expands or perhaps not.

In the two cases, the combination off rising credit cost and the need to obtain additionally big date tend to compound the debt burden and you will consume aside at collateral yourself; leaving shorter if the citizen motions or becomes deceased.

Reckoning has begun for individuals whom tap into their house security

In addition to eating away from the collateral within the Canadian belongings was dropping possessions opinions, and therefore we are currently seeing since the Lender regarding Canada nature hikes pricing so that you can rein within the rising prices.

Where this might potentially end up being going are stunning due to the popularity of home security finance. They are something of 3 decades off stone-base interest rates and you may have not been checked-out against the double-fist rates of interest of your own 1980s.

Meanwhile, the fund business continues to discover an approach to utilize domestic-steeped Canadians as they get older. Canada’s banking regulator, any office of your Superintendent of Loan providers (OSFI), is reportedly scrutinizing the newest domestic security borrowing equipment titled an excellent readvanceable financial, which combines a timeless financial with a personal line of credit one the gains given that resident pays on the dominant.

The latest expanding loans levels of Canadians, yet not, are a reduced amount of a problem to possess OSFI (in addition to money globe) than their ability to service one to debt. Canadian financial institutions try renowned to own handling risk and is likely that house collateral borrowing limits will remain conveniently beneath the appraised value of our home.

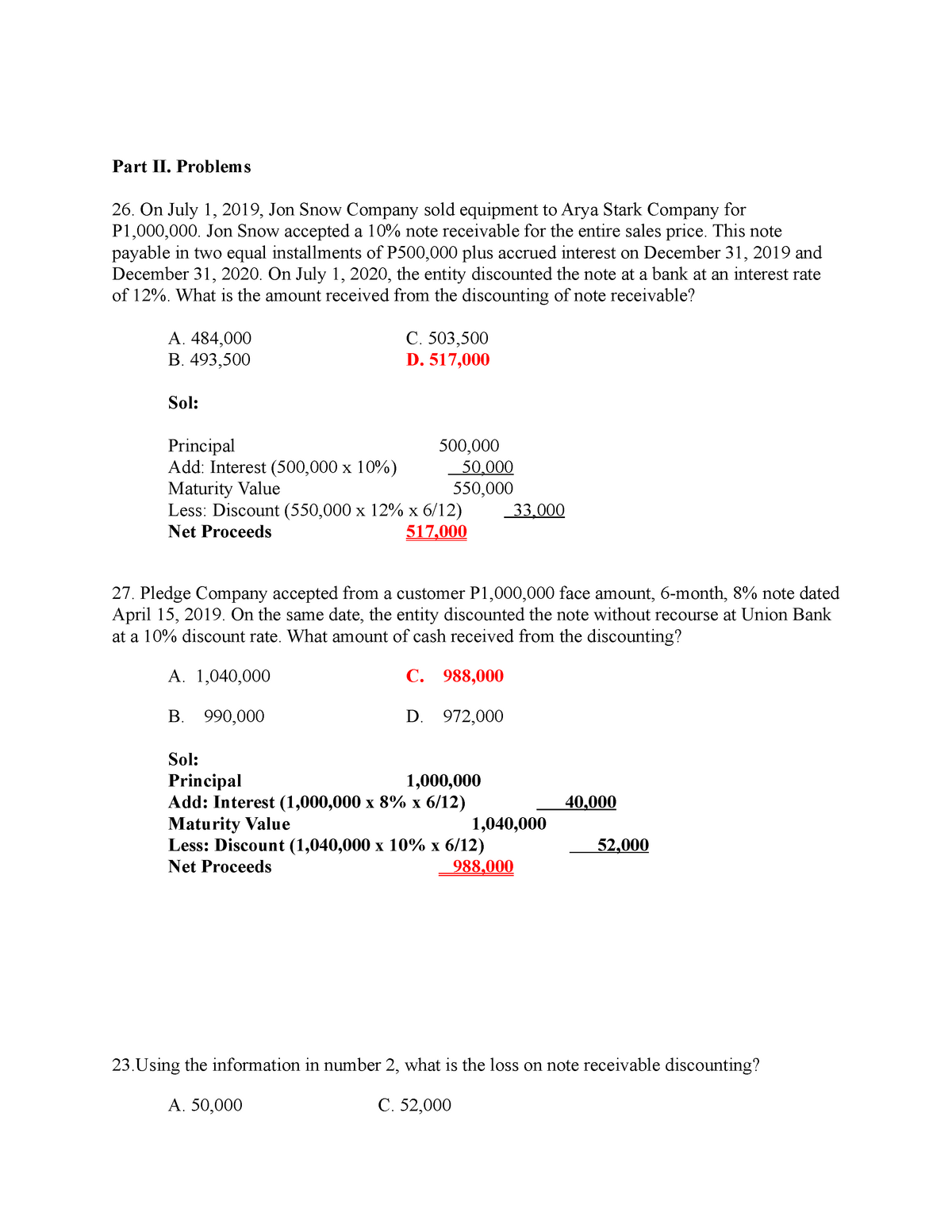

This is the elderly home owners sinking better indebted that will become the press. Significantly less than Canadian legislation, loan providers are unable to confiscate a house; however, as they need more cash to meet up with cost of living, and desire money build, elderly people will be compelled to market to safety the funds otherwise leave virtually no security to own beneficiaries after they pass away.